Industry Research: Competing Home Improvement Stores’ Market Strategy

The Home Improvement sector is dominated by two companies - Home Depot and Lowe’s. Broadly speaking, companies in this industry can look to differentiate on location, price, and product selection.

We honed in specifically on location. We wondered - How do these two brands that sell effectively the same products at similar price points choose to locate? What do their locations suggest about their location strategy and the competition in the industry?

Key Findings

Home Depot has ~250 more stores than Lowe’s in the United States and has higher concentration in California, New York, and Georgia. Lowe’s has higher store concentration in North Carolina and Ohio.

Home Depot’s location advantage is largely a result of building more density in a given market versus opening in different markets than Lowe’s.

The brands have highly overlapping location strategies.

The median distance from a Lowe’s to the closest Home Depot is <2.5 miles.

Growth opportunities are unlikely to come from significant store count growth; we see higher opportunity in exploring alternate store formats to enable new market opportunity.

Store Count and Geographic Insights

Home Depot has the advantage in store count in the United States with about 250 more stores than Lowe’s. Geographically, we see modest differences in where stores are located.

Home Depot has their highest number of stores in California, which is 4th highest for Lowe’s. New York and Georgia also appear in the top 5 for Home Depot while North Carolina and Ohio appear in the top 5 for Lowe’s.

Important to note here is that Home Depot is headquartered in Atlanta and Lowe’s in Charlotte, NC, likely leading to higher location count in the respective states.

At the state level, of the 50 US states plus DC where both brands operate, Home Depot has a higher store count in 29, Lowe’s in 20, and the two have the same store count in 2.

Adjusted for population, Lowe’s has the highest number of stores in North Carolina and Home Depot in New Hampshire. Other states of note for Lowe’s are Kentucky, West Virginia, and South Carolina. For Home Depot is Wyoming, Alaska, Georgia, and Connecticut.

When looking at the store locations themselves, we see Lowe’s has much higher clusters of stores along the East Coast and into the Midwest, while Home Depot has more locations scattered through the center of the country.

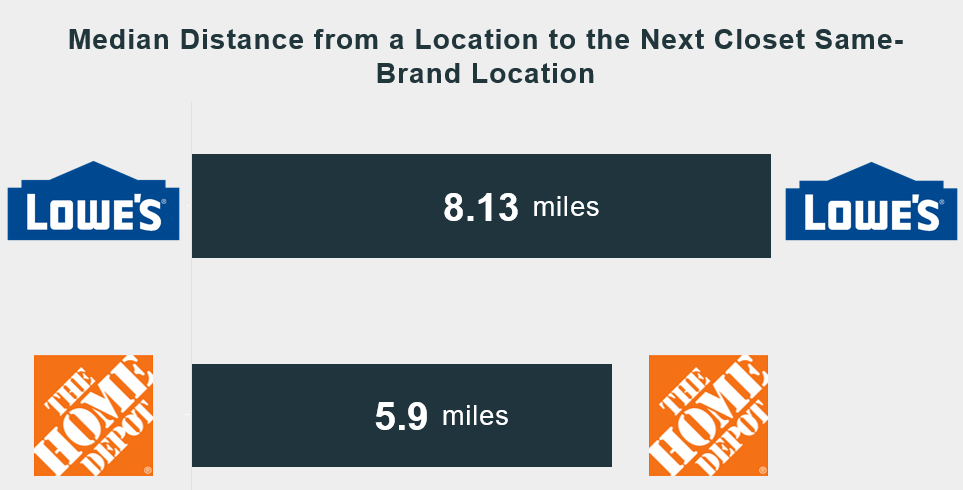

Although the map for Home Depot appears to show more isolated locations, the data suggests it builds more density in markets than Lowe’s. The median distance from one Home Depot store to the next closest Home Depot is just 5.9 miles, while the distance from Lowes to its next closest store is 8.1 miles.

Head-to-Head Location Intelligence

Going a layer deeper, we can look at the two brands and their interaction with each other. Within a market, do they locate in similar places or different?

The answer to this question is that there’s remarkably high overlap between the locations of the two brands.

Said another way - when you see a Lowe’s or Home Depot, there’s a very high likelihood that the other is nearby.

Half of Lowe’s locations have a Home Depot within 2.23 miles and 77% have a location within 10-miles.

This suggests that either (1) the brands see themselves as going after different customers in the same market or (2) they compete head-to-head for the same customers in the same places.

Anecdotally, there’s a perception that Home Depot caters more to contractors and professionals while Lowe’s is more friendly to the average homeowner, but we wouldn’t think the difference is substantial enough to suggest low overlap in customer base.

Instead, the second explanation is more likely — good old fashioned competition in a market. We frequently see examples in the data where the brands are right next to each other, forcing a customer to decide on one or the other.

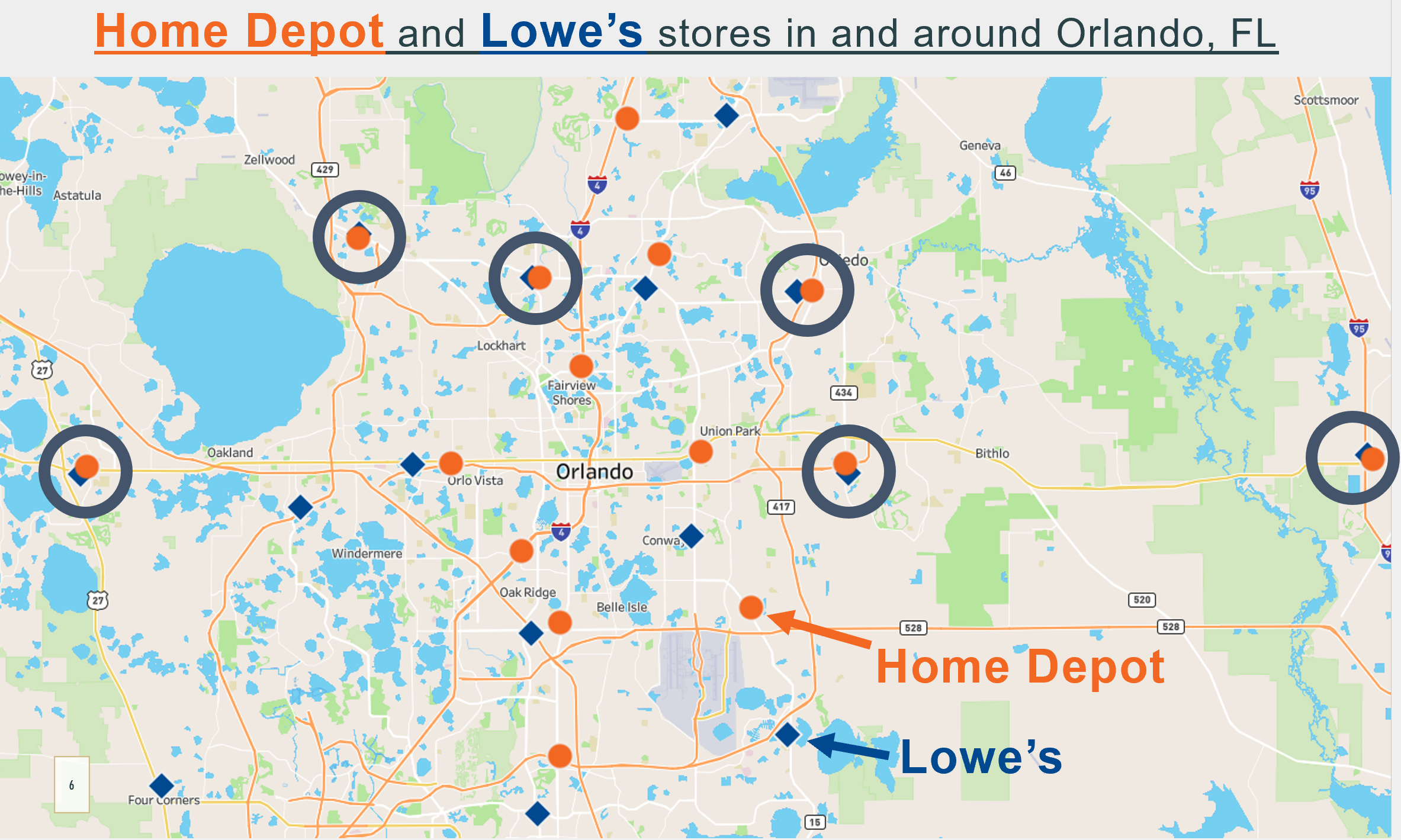

Consider the example below in Orlando and the surrounding area. There are 6 competing stores in just this market where Lowe’s and Home Depot are less than 0.5 miles from each - and sometimes much closer than even that.

Thus, our analysis suggests that the brands largely don’t differentiate on location selection but compete in the same places with slightly different - but similar - customer focus.

Home Depot’s location advantage is a result of (1) building more stores in the same markets and (2) a willingness to open in less populous markets where we’d estimate the area can’t support both stores operating.

The first point is evident in a market like greater San Francisco, where both brands have a footprint. In the same area, Home Depot operates over twice the amount of stores than Lowe’s. In particular, look at the area running down the coast East of San Francisco from Richmond to Milpitas.

In this area, Home Depot has a methodical location strategy. These stores are all 5-7 miles apart and convenient from the highway.

Lowe’s has just two locations on this same stretch - both very close to the Home Depot locations.

On our second point, we see a high differential of Home Depot and Lowe’s stores in locations with lower population and less population density. In states like New Hampshire, Alaska, Wyoming, and Minnesota, we see differentiation between the presence of the two brands.

Our hypothesis is that Home Depot was first to open in the suburban-rural areas of these states, and the market size doesn’t justify both brands operating in a nearby space.

Closing Thoughts

Location strategy is just one lever brands can use to differentiate from their competition. Here, we see that the two home improvement brands largely find building density and competing head-to-head to be a better strategy than finding new whitespace opportunities.

There seems to be an element of estimating how many big box home improvement stores an area can support, then building density in the market until that number of stores is reached.

Neither of these brands is poised for explosive location growth. The size and scale of their locations makes finding the right real estate challenging, and most markets that can be meaningfully penetrated already have been.

Instead, there’s value in pursuing growth through testing alternative store formats to grow the market opportunity.

Lowe’s has been experimenting with Outlet stores to sell “slightly imperfect” new appliances at discount prices. This is a distinct business model and value proposition compared to their traditional stores, presenting an opportunity to open in new markets or alongside current stores without high cannibalization.

Perhaps one of the brands may also take a page out of Target’s book and test smaller format stores in city centers to capitalize on large markets that don’t have the traditional size required for a new store. Today, large markets like DC have only 1 store for both brands, but undoubtedly the demand for home improvement supplies is higher in the city than the location count suggests.

Rather, finding the amount of space needed for a traditional store is infeasible in dense urban environments.

When the runway for the current strategy starts to run low, brands can benefit from exploring alternate ways to drive value for their customers through new store formats or avenues to continue to reach a wider audience.

Interested in this topic? Get in touch with me here or by email at jordan@jordanbean.com.